NZ Business Survey and China Trade Data Put Recovery to the Test

Tuesday's Asia calendar features two policy-relevant releases: New Zealand's Q2 business survey and China's June trade figures ahead of Wednesday's GDP.

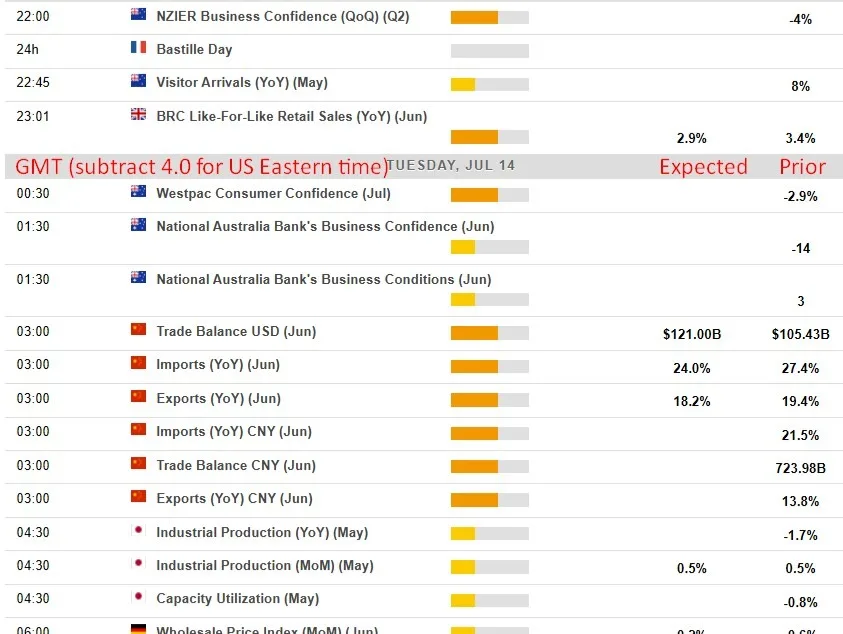

Two closely watched data releases hit Tuesday's Asia session with real policy stakes. New Zealand's NZIER Quarterly Survey of Business Opinion drops at 2200 GMT, followed by China's June trade figures around 0300 GMT — both arriving as economists question how durable recent improvements in sentiment and trade flows actually are once wartime distortions are stripped away.

The NZIER survey is drawing attention not for its headline number but for what's inside it. The Q2 survey window straddled the mid-June Iran ceasefire, meaning a split between early and late responses could reveal far more than any blended average. Westpac is watching whether pricing intentions stayed elevated even as oil pulled back toward pre-conflict levels — a persistent inflation signal that would complicate the Reserve Bank of New Zealand's case for further rate cuts. ASB, meanwhile, is focused on capacity measures after Q1 data showed labor emerging as a tighter constraint and firms raising selling price expectations for a second straight quarter.

Read more The 10 Worst-Performing State Economies in the US for 2026 →

China's trade print carries its own weight as a lead indicator into Wednesday's GDP release. Exports are forecast to cool modestly to 18.2 percent year-on-year from 19.4 percent in May, while imports are expected to slow to 24 percent from 27.4 percent. South Korean export data suggest demand remains concentrated in semiconductors rather than reflecting a broad domestic consumption recovery — a distinction markets will scrutinize. Forecasts diverge sharply, with some international banks projecting export growth near 20 percent while cautious domestic Chinese research houses pencil in figures as low as 12 percent. The trade surplus is seen widening to roughly $120.6 billion.

A soft imports reading alongside resilient exports would reinforce a persistent worry: that external demand, not domestic consumption, is still doing the heavy lifting in China's economy. For the RBNZ, any sign that inflation pressures outlasted the geopolitical shock that briefly amplified them would shift the rate outlook in a less dovish direction. Both releases land before most Western markets open, giving Asian traders first mover advantage on the narrative.

Continue reading at Forexlive.